JD.com Q3 2025: Profitability Under Pressure, New Businesses Emerge as Growth Drivers

JD.com (NASDAQ: JD) recently released Q3 2025 financial results, which show year-on-year revenue growth but a decline in profits. At the same time, the proportion of various business segments has shifted: while new businesses remain small in absolute terms, their revenue has grown by over 300% YoY, and service revenue has also shown strong growth.

Ⅰ. Overall Performance: Slowing Revenue Growth and Declining Profitability

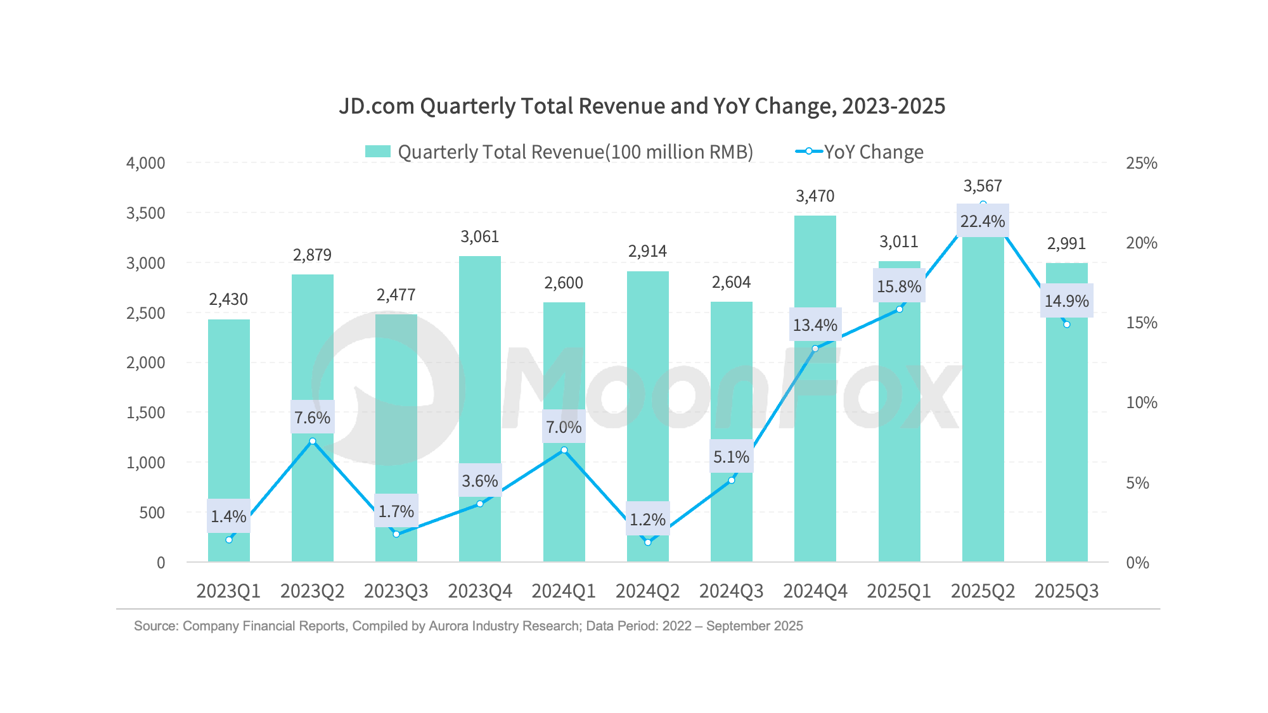

In Q3, JD.com achieved total revenue of RMB 299.1 billion, up 14.9% YoY. After four consecutive quarters of accelerating growth, this quarter marks the first slowdown, though performance remains solid compared to previous years.

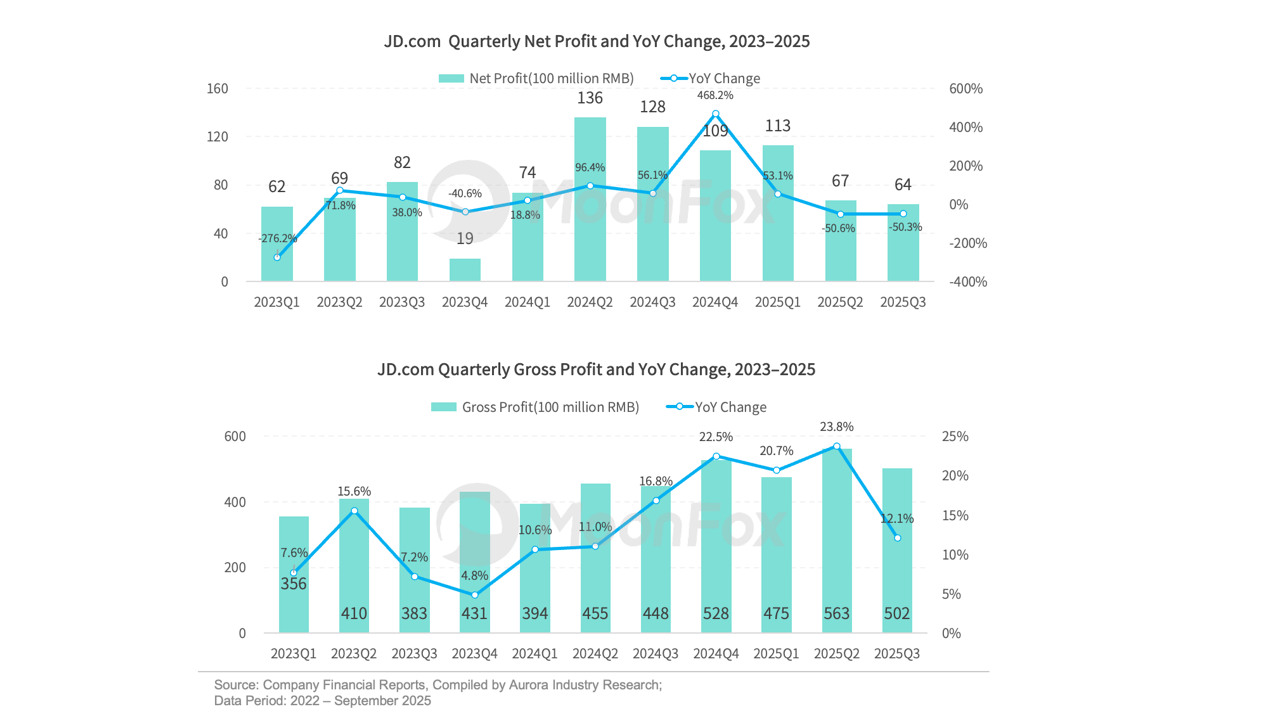

Looking at historical data, since Q2, JD.com’s net profit has fallen back to 2023 levels, and continued to decline in Q3, with a YoY drop of over 50%.

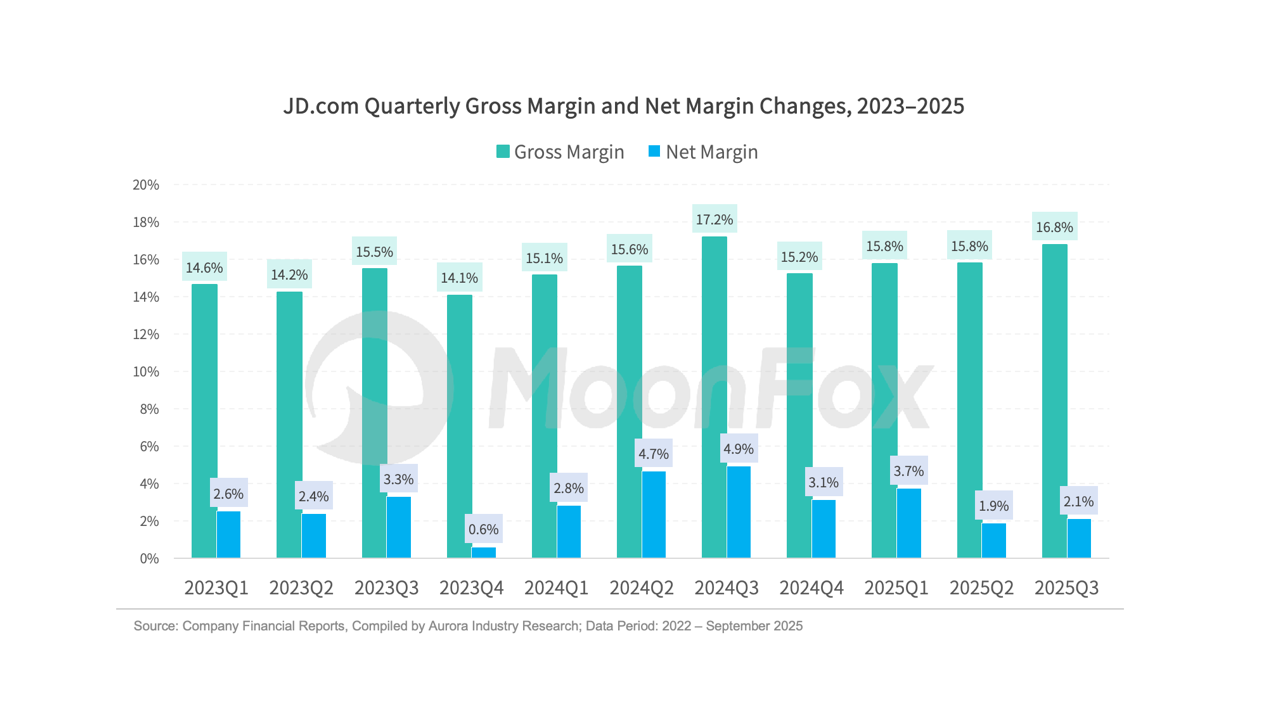

Gross margin in Q3 was 16.8%, down 0.4 percentage points YoY. While this is an improvement from Q2’s 15.9%, it remains relatively low. Net margin dropped sharply from 4.7% last year to 2.1%. Operating income has been negative for two consecutive quarters, highlighting the severe challenge of balancing cost control and profitability.

Ⅱ. Cost Analysis: Surging Marketing and Fulfillment Expenses Drive Losses

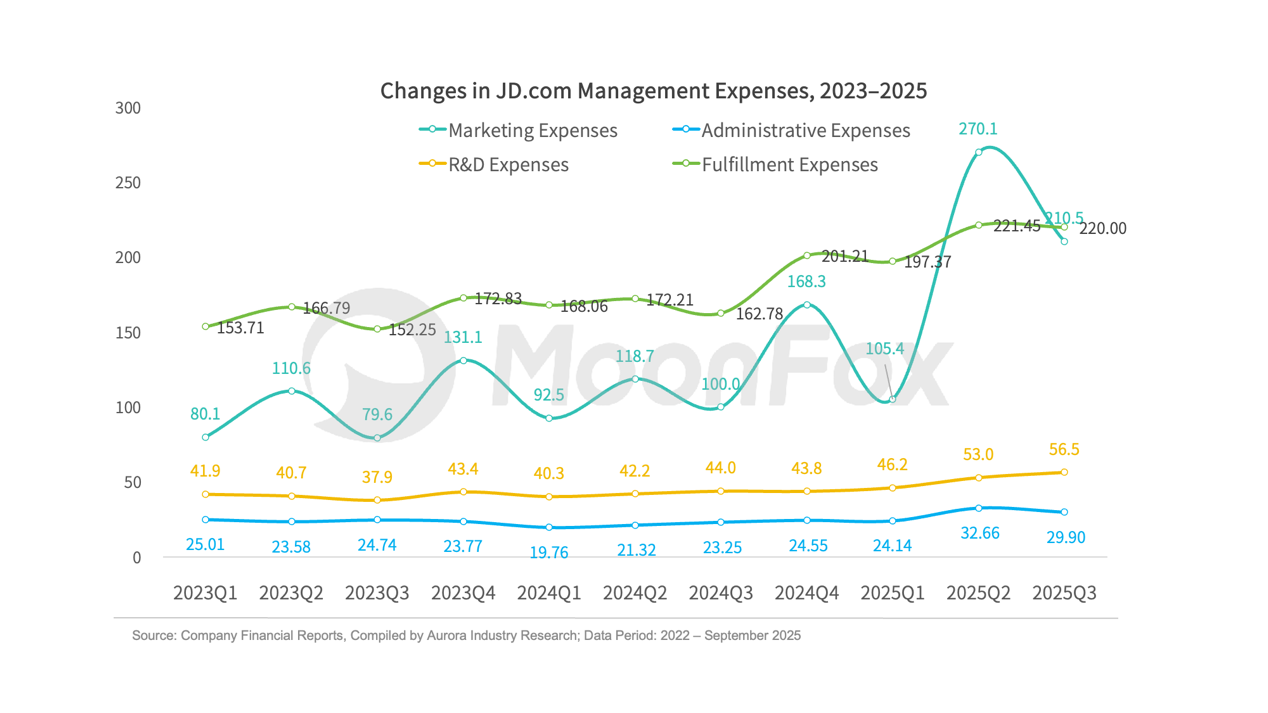

JD.com’s Q3 operating costs reached RMB 248.6 billion, up 15.4% YoY, slightly outpacing revenue growth. The total of the four major management expenses (R&D, administrative, fulfillment, and marketing) reached RMB 31.7 billion, up about 55% YoY—far exceeding the 14.9% revenue growth, and a key reason for the swing to operating losses.

A deeper analysis of quarterly management expenses reveals that the main drivers of declining profitability are the surges in marketing and fulfillment costs:

Marketing expenses were the biggest culprit for profit decline, reaching RMB 21.05 billion this quarter, up 110.5% YoY. The ratio to revenue jumped from 3.8% last year to 7.0%. This growth far outpaces revenue, mainly due to market promotion and user acquisition for new businesses, especially food delivery. The sharp increase in marketing expenses reflects fierce competition in instant retail and local services.

Fulfillment expenses also grew rapidly, reaching RMB 22 billion, up 35.2% YoY. The ratio to revenue increased from 6.3% last year to 7.4%. The rise in fulfillment costs is mainly due to JD.com’s ongoing optimization of its fulfillment capabilities and increased investment in manpower to enhance user experience, particularly in building instant delivery networks.

R&D expenses were RMB 5.6 billion, up 28.4% YoY, accounting for 1.9% of revenue. Administrative expenses were RMB 3 billion, up 28.6% YoY, accounting for 1.0% of revenue. While both R&D and administrative expenses increased in absolute terms, their scale and proportion remain manageable.

Ⅲ. Business Analysis: Faster Growth in New Businesses, Stable Core Performance

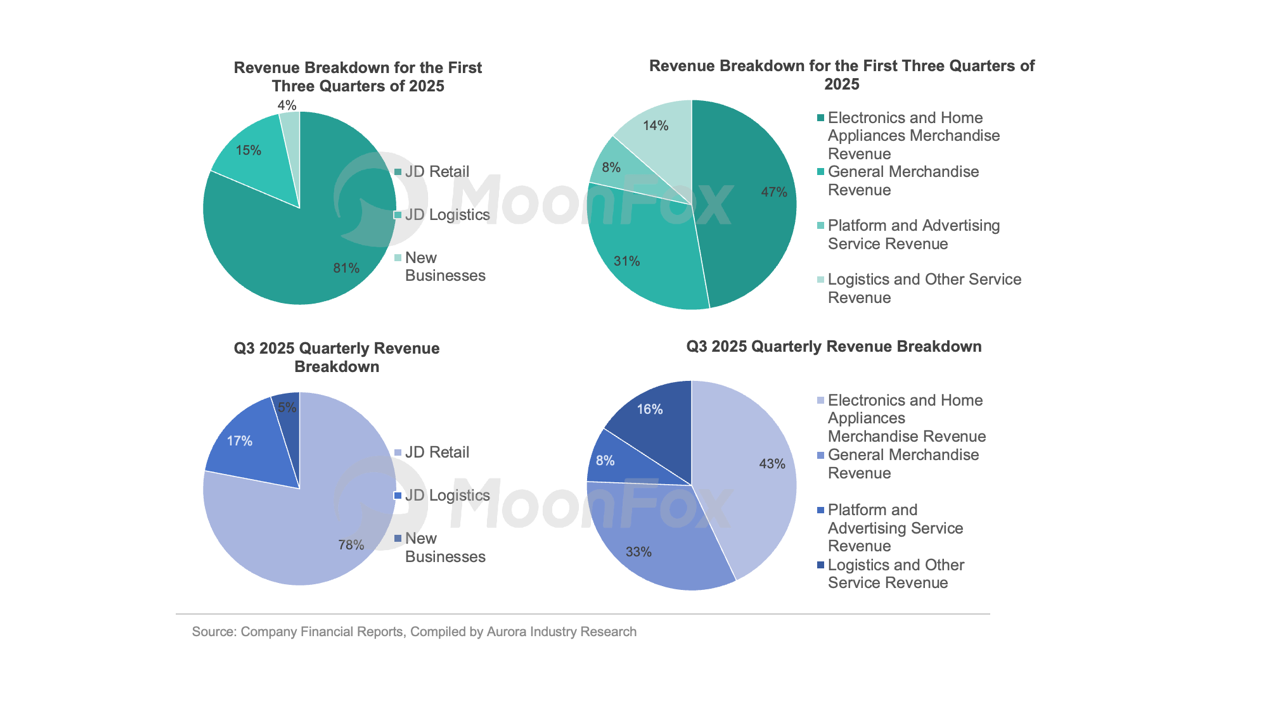

In the first three quarters of 2025, the proportion of service revenue increased by 2 percentage points YoY, while the proportion of merchandise revenue fell by 2 percentage points.

Q3 2025 merchandise revenue was RMB 226.1 billion, up 10.5% YoY, accounting for 76% of total revenue. Service revenue was RMB 73 billion, up 30.8% YoY, with its share rising to 24%. The strong growth in service revenue was mainly driven by platform and advertising services (RMB 25.7 billion, up 23.7% YoY) and logistics and other services (RMB 47.3 billion, up 35.0% YoY). This optimization of revenue structure reflects JD.com’s gradual transformation from a traditional merchandise retailer to a service-driven new retail enterprise.

By business type, JD Retail and Logistics maintained relatively stable YoY growth rates and stable revenue proportions in the core business. New business revenue totaled RMB 35.2 billion YTD, doubling YoY and increasing its share by 1.8 percentage points. New businesses were a key growth highlight for JD.com in 2025, especially evident in Q3.

Q3 2025 JD Retail revenue was RMB 250.6 billion, up 11.4% YoY; JD Logistics revenue was RMB 55.1 billion, up 24.1% YoY, demonstrating strong supply chain service capabilities. New business performed most impressively, with revenue of RMB 15.6 billion, soaring 213.7% YoY.

Ⅳ. Business Development: Strengthening Retail, Accelerating New Business and AI Product Development

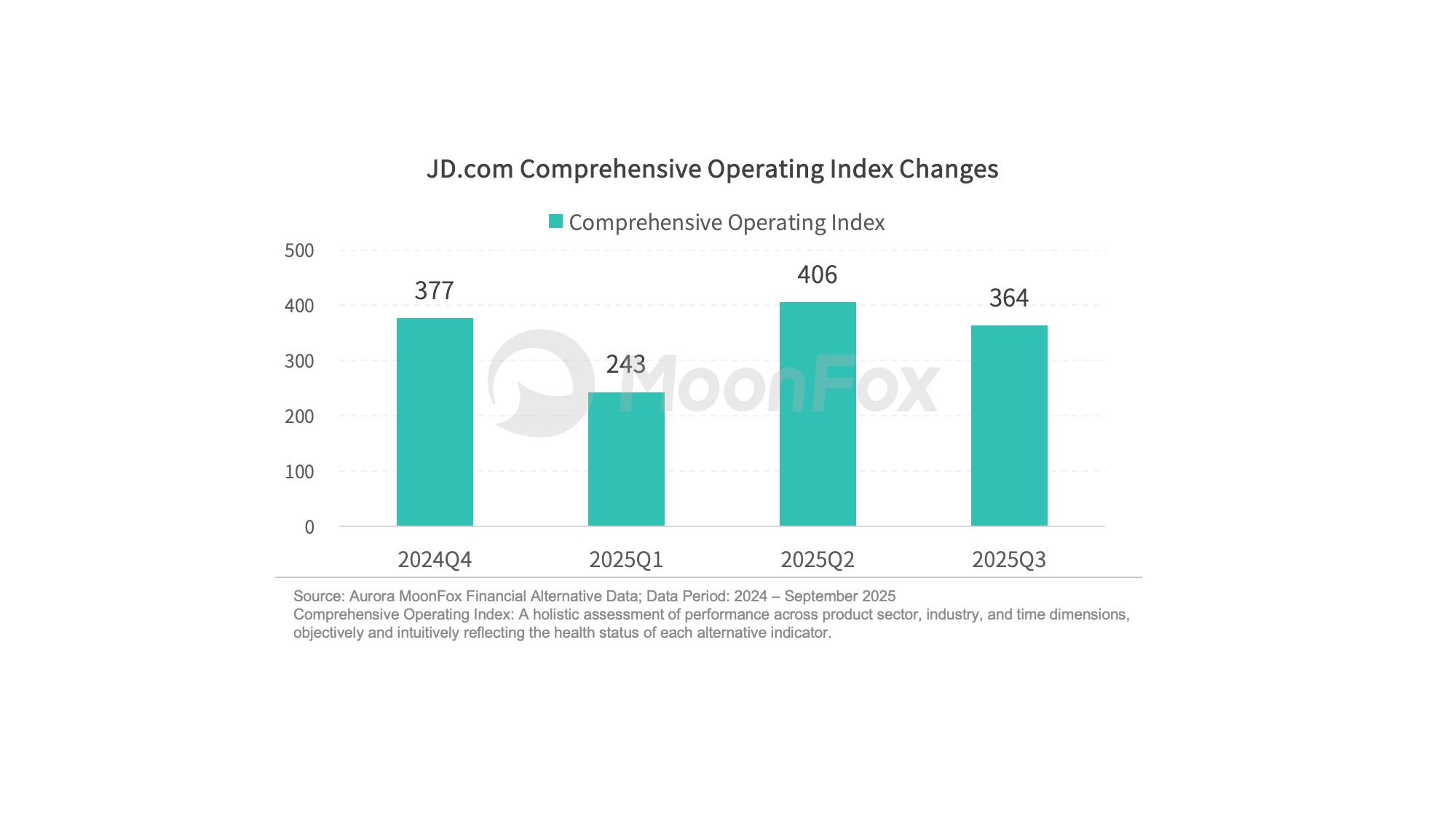

According to Aurora MoonFox alternative financial data, JD.com’s comprehensive operating index declined in Q1 2025 compared to the end of 2024, but saw significant growth in Q2 and Q3. The comprehensive operating index is mainly affected by fluctuations in the scale of app online users. After accelerating the layout of life services in February 2025, user traffic on the online platform was significantly stimulated. However, this data trend aligns with quarterly revenue but does not fully correspond to changes in profit. Overall, JD.com’s offline and life services businesses are still in the early stages of development, with significant strategic investment costs constraining profitability to some extent. However, as AI technology is implemented in vertical sectors and the integration of online and offline retail networks continues, these investments are expected to benefit the company’s long-term development, though the extent of synergy and profit contribution remains to be seen.

In 2025, JD.com continued to expand its offline stores, accelerating the integration of online and offline retail service networks. Offline retail operations focus on store management, supply chain management, and warehousing logistics, deeply integrating with online channels to achieve “omnichannel retail.” The asset-light property model—acquiring properties through leasing—helps control costs. By the end of Q3, JD MALL operated over 20 stores nationwide, and JD Electronics city flagship stores exceeded 100. In September 2025, JD.com reached a strategic partnership with China Resources Land, announcing that Hong Kong’s first JD MALL will open in Wan Chai’s core area in 2026, marking the company’s offline expansion from mainland China to overseas markets.

JD.com’s strategic investment in AI is empowering the supply chain and vertical businesses, with positive effects gradually emerging. In July, at the 2025 World Artificial Intelligence Conference (WAIC), JD.com upgraded its large model brand to JoyAI and open-sourced JoyAgent, the industry’s first 100% enterprise-grade intelligent agent. In September, JD Health signed a strategic cooperation agreement with Union Hospital, Tongji Medical College, Huazhong University of Science and Technology, to jointly promote the application of JD Health’s “JD Zhuoyi” AI product in offline hospital clinics, building a full-process AI-assisted consultation system. The two parties will also deepen cooperation in internet medical services and medical education, exploring new models of “Internet + Healthcare” services.

The Q3 earnings report mentioned that JD.com’s food delivery business has significantly boosted retail user growth, shopping frequency, and cross-category consumption. Meanwhile, new business expansion is extending from food delivery to travel and housekeeping services, gradually forming a comprehensive local lifestyle service network. In mid-November, JD.com launched an independent “JD Delivery” app, which not only provides food delivery and instant retail services but also aggregates local store reviews and recommendations. In the future, JD.com aims to retain more users, activate its content community, and use content to drive more business.

About MoonFox Data

MoonFox Data, a subsidiary of Aurora Mobile (NASDAQ: JG), is a leading alternative data provider delivering actionable insights to global financial institutions and investment firms. Trusted by top 50 funds, MoonFox leverages proprietary big data and advanced analytics to help clients uncover market trends and drive smarter decisions across China and emerging markets.

5月应用百强榜单出炉!AI应用持续升温,消费服务赛道表现亮眼

2026年一季度小鹏汽车:利润转好昙花一现,市场地位下滑迅速